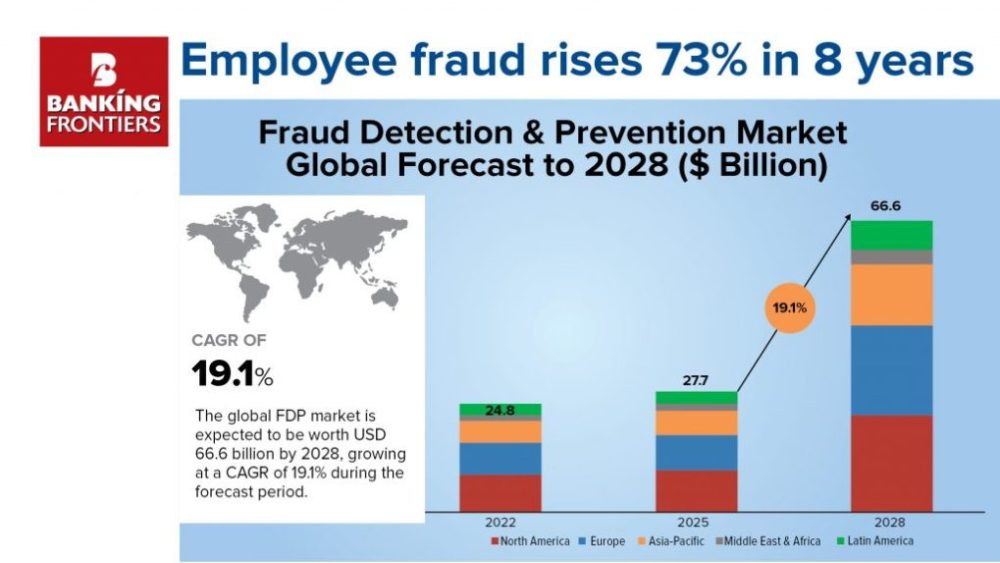

Employee fraud rises 73% in 8 years

2 minute read.

In recent years, employee fraud has surged dramatically, with incidents increasing by a staggering 73% over the past eight years. This alarming trend highlights a growing concern for businesses and organizations, as internal dishonesty becomes a more prevalent threat to financial stability and trust. As companies face this escalating risk, understanding the underlying causes and implementing effective preventative measures are more crucial than ever. This article delves into the factors driving the rise in employee fraud and explores strategies to combat this pervasive issue.

Imagine this: you entrust your hard-earned savings to a financial institution, only to discover an employee has siphoned them off to fuel a gambling habit or extravagant lifestyle. Fortified brick walls, intricate security systems, and watertight protocols – these are the bulwarks that banks and insurance companies have traditionally relied upon to safeguard themselves and their clients. But what if the enemy lies not outside, but within? This isn’t a fictional thriller; it’s the harsh reality of employee fraud, a cancer gnawing at the heart of the finance sectors globally.

Employee fraud is a complex issue with no easy solutions, says Agatha Li, CEO of the Hong Kong Institute of Bankers.

While pinpointing the exact locations of these betrayals is difficult, certain areas emerge as hotspots. In the US, Florida reigns supreme, accounting for a whopping 22% of all bank fraud cases between 2016 and 2020. Looking abroad, China, India, and Brazil consistently rank high in global fraud reports.

A Global Menace

Across the globe, the number of reported employee fraud cases in the financial sector has been steadily rising. According to a 2023 report by the Association of Certified Fraud Examiners (ACFE), global occupational fraud losses reached a staggering $42 billion, with a median loss of $150,000. The numbers paint a grim picture. According to a 2023 study by PwC, global financial institutions witnessed a staggering 40% increase in occupational fraud between 2018 and 2022. In India alone, the Reserve Bank of India reported Rs. 302.5 billion in bank frauds for the fiscal year 2022-23, a decrease from the previous year’s staggering Rs. 1.3 trillion, but still indicative of a significant problem. While India grapples with its fair share of cases, countries like the UK, the US, and Luxembourg haven’t escaped unscathed. In fact, a recent report found that the median loss per occupational fraud case in the US reached a record high of $243,000 in 2022.

Imagine 1.2 million branches worldwide, each with a potential vulnerability. Now, consider this: reported employee fraud cases ballooned by a staggering 73% between 2013 and 2021. That’s not chump change; these thefts amounted to a collective $42.2 billion stolen in the US alone. The international landscape paints a similarly concerning picture. The international landscape paints a similarly concerning picture. In 2023, a former Bank of China manager was jailed for life for a $322 million heist, while India witnessed a Rs. 25 crore bank employee fraud.

While employee fraud plagues institutions worldwide, certain regions and cities seem to be particularly afflicted. Within India, specific cities and states seem to be more susceptible to employee fraud. Maharashtra, for instance, reported the highest number of bank fraud cases in 2022-23, followed by Karnataka and Tamil Nadu with several high-profile cases involving employee misconduct. Globally, Luxembourg, Nepal, and the UK also witnessed notable incidents. This geographical analysis underscores the need for targeted mitigation strategies that consider regional vulnerabilities and cultural nuances.

But the true cost goes beyond mere rupees and cents. It erodes trust, weakens financial stability, and tarnishes the reputation of the entire industry. So, where are these vulnerabilities lurking, and what can be done to fortify our defences?

Insurance industry under siege

The insurance sector isn’t immune either. A 2023 report by the Insurance Regulatory and Development Authority of India (IRDAI) revealed ‘1088 cases of mis-selling’ by insurance agents in the previous year, often driven by employee incentives and pressure to meet targets. This unethical practice not only harms customers financially but also erodes trust in the entire insurance ecosystem.

However, the story doesn’t end there. The rise of digitalization has opened new avenues for employee misconduct. From manipulating online transactions to exploiting cyber security loopholes, tech-savvy fraudsters are finding increasingly sophisticated ways to exploit their insider access.

Evolving Modus Operandi

The methods employed by these insider threats are as diverse as their motivations. From classic embezzlement and loan scams to cyber-enabled fraud exploiting internal systems, the perpetrators are constantly evolving their tactics. A recent case in Mumbai saw a bank employee siphon off gold and cash from customer lockers, highlighting the audacity and creativity of these fraudsters.

The methods employed by these rogue employees are as diverse as their motivations. Account manipulation, identity theft, and fraudulent loan schemes are common tactics. Worryingly, technology is becoming a double-edged sword: digital channels like mobile banking offer new avenues for exploitation.

Dual-Pronged Defence

So, how can finance institutions fortify their defences against this ever-growing threat? A two-pronged approach is crucial: prevention and detection. Implementing robust internal controls, segregation of duties, and regular audits are essential first steps. But in today’s dynamic landscape, advanced analytics and AI-powered fraud detection systems are becoming increasingly critical in identifying anomalies and uncovering suspicious activity before it’s too late.

The complexity and sophistication of these attacks necessitate a multi-pronged approach, says Amitabh Chaudhary, MD & CEO, Axis Bank. He says banks must invest in robust cybersecurity infrastructure, conduct regular employee training, and foster a culture of ethical conduct.

Banks are increasingly leveraging advanced technologies, with a predominant focus on artificial intelligence (AI) to fortify their defence mechanisms. Recent insights gleaned from various sources highlight the industry’s proactive measures in combating the surge in sophisticated financial crimes. The integration of AI in fraud detection and prevention has become a cornerstone strategy for banks and payment firms. As articulated in the Fintech Magazine article, AI is emerging as a powerful tool to protect against bank fraud scams, showcasing its efficacy in identifying and mitigating evolving threats.

The deployment of AI-driven solutions is particularly pertinent amid the rising tide of peer-to-peer frauds and scams, necessitating unique and adaptive approaches as elucidated in The Financial Brand’s report. This concerted effort is echoed in Nordea’s perspective on tackling fraud in the new banking landscape, underscoring the industry’s commitment to staying ahead of the curve. The proactive stance is further validated by a study highlighted in Banking Exchange, indicating a significant investment by banks in technology to bolster their defences against fraud. As the industry forges ahead, the amalgamation of cutting-edge technology and strategic risk management remains imperative in safeguarding the integrity of financial institutions and fostering a secure banking environment.

Beyond Technology

Technology alone cannot win this battle. Fostering a culture of ethics, transparency, and accountability within organizations is equally important. Investing in employee training, promoting whistleblowing mechanisms, and addressing internal pressures that might incentivize fraudulent behavior are crucial steps in building a strong ethical foundation.

Collaboration between banks, regulators, and law enforcement is vital to share best practices and apprehend criminals. David Evans, Chairman of the Association of Foreign Banks in India, echoes this sentiment, and emphasizes that investing in employee education and ethical training is crucial. He avers the need to cultivate a culture of integrity within the organizations.

Call to Action

The fight against employee fraud demands a united front. Collaboration between industry players, regulators, and law enforcement agencies is essential for sharing best practices, identifying emerging trends, and bringing perpetrators to justice. The recent arrest of a gang operating across multiple banks in Haryana signifies the power of such cooperative efforts.

Employee fraud is a hydra-headed monster, demanding constant vigilance and innovation. By staying ahead of the curve, leveraging technology ethically, and fostering a culture of trust, leaders can safeguard their institutions and rebuild customer confidence. The battle lines are drawn. Will the guardians of finance prevail, or will the silent threat continue to erode the very foundation of the industry? The answer lies in their collective action.

The Above Araicle for first published in Bandking Frointers –